The Difference Between Looking Rich and Becoming Wealthy

Why ownership creates lasting wealth while appearances often hide financial fragility.

Welcome to today’s read; let’s make this simple and useful.

A luxury watch can tell the time. A diversified portfolio can buy it.

These days, wealth has become increasingly visible.

Scroll through Instagram, X, or YouTube, and you will find people documenting business-class flights, luxury cars, designer handbags, expensive restaurants, and dream homes. The message is subtle but powerful: this is what success looks like.

But there is a problem.

What looks like wealth is often consumption. Actual wealth is ownership.

The distinction matters because millions of people around the world are working harder than ever to improve their lives, yet many are directing their highest-earning years toward assets that impress others rather than assets that improve their own financial future.

This isn’t an argument against enjoying money. It is about understanding the difference between displaying financial success and building it.

The two often look similar in the short run. Over decades, they lead to completely different outcomes.

Looking Rich Is About Income. Becoming Wealthy Is About Net Worth.

Most people judge financial success by visible signals.

The house.

The car.

The clothes.

The vacation photos.

Financial professionals look somewhere entirely different.

They start with one question:

What is your net worth?

Most people know their salary. Many know the balance in their bank account. Surprisingly few know their net worth.

Your net worth is the total value of everything you own minus everything you owe. That includes your investments, cash, property, retirement accounts, business interests, and other assets, after subtracting loans, mortgages, credit card balances, and other liabilities.

Think of it as your personal balance sheet. Unlike your income, which measures how much money comes in each year, your net worth measures how much wealth you have actually built.

This distinction matters because income can disappear if you stop working. A growing net worth, however, represents assets that can continue to generate income, appreciate in value, or support your lifestyle independently of your next paycheck.

Income determines your lifestyle today.

Ownership determines your options tomorrow.

That distinction is easy to miss because income is visible while ownership usually isn’t.

Visible Wealth Is Designed to Be Seen. Invisible Wealth Is Designed to Grow.

There is an interesting paradox in finance.

The assets people notice are often the least important contributors to long-term wealth.

The assets that matter most are usually invisible.

No one notices:

Index fund contributions

Business equity

Retirement accounts

Dividend reinvestment

Cash reserves

Private ownership stakes

These rarely appear in photographs.

Yet these are the assets that generate future income.

Economists often describe wealth through household balance sheets rather than visible possessions because balance sheets reveal productive assets and liabilities, not appearances. Research comparing household wealth data consistently shows that net worth, not consumption, is the meaningful measure of financial strength.

A luxury car can create attention.

An ownership stake in a profitable company can create income for decades.

One depreciates.

The other may compound.

That difference changes everything.

Status Spending Creates Signals. Ownership Creates Cash Flow.

Humans have always used possessions to communicate status.

Luxury brands understand this psychology exceptionally well.

Many products are valuable not because they perform better, but because other people recognise them.

Economists sometimes call these positional goods, products whose value depends partly on being seen.

Ownership works differently.

Owning productive assets means owning future cash flows.

Consider the difference between buying:

a designer handbag

shares in a company that manufactures designer handbags

The first consumes capital.

The second may generate future returns if the business succeeds.

The same logic applies across industries.

Owning rental property.

Owning shares.

Owning a business.

Owning intellectual property.

Owning royalties.

Ownership shifts money from consumption toward production.

That is why many wealthy families spend far more time discussing businesses than brands.

The Biggest Financial Trap Isn’t Low Income. It’s Lifestyle Inflation.

One of the least discussed risks in personal finance is that higher income often increases spending faster than wealth.

This phenomenon appears repeatedly across countries.

Recent reporting on high-income Indian households found that many affluent earners save surprisingly little because rising income is matched by rising lifestyles, expensive financial products, and social expectations.

The pattern isn’t unique to India.

It exists in New York.

Dubai.

London.

Singapore.

Sydney.

Income rises.

Housing becomes larger.

Cars become newer.

Vacations become more expensive.

Subscriptions multiply.

Normal schools replace expensive schools.

Soon, a family earning twice as much discovers they still feel financially constrained.

The problem isn’t earnings.

It’s that expenses evolved to consume every increase.

Financial freedom requires creating a gap between income and lifestyle.

That gap becomes invested capital.

Invested capital becomes future freedom.

Some People Look Wealthy But Are Financially Fragile

We have all met someone who seems rich.

They live in an expensive neighbourhood, drive a luxury SUV, wear designer watches, and take international vacations every year.

Yet if they suddenly lost their job or faced a large medical bill, they might struggle to cover a few months of expenses without borrowing.

That isn’t unusual.

Economists even have a name for this group: the “wealthy hand-to-mouth.” These are households that own valuable assets, such as homes or retirement savings, but keep very little cash or other liquid investments available for emergencies. Studies have found this pattern across many developed economies, including the US, Canada, the UK, Germany, France, Italy, Spain, and Australia.

The lesson is simple but often overlooked: owning expensive assets is not the same as being financially secure.

Liquidity rarely attracts attention, but it is often what determines whether a financial setback becomes a minor inconvenience or a major crisis.

Having assets that cannot easily be converted into spending money creates a very different financial reality than having diversified, accessible investments alongside long-term assets.

A strong balance sheet isn’t only about total wealth.

It’s also about flexibility.

Social Media Changed the Economics of Looking Rich

Before social media, status was mostly local.

Your neighbours compared themselves with other neighbours.

Today, everyone compares themselves with celebrities, entrepreneurs, influencers, athletes, and strangers whose financial lives are largely unknown.

Algorithms amplify visual consumption.

Nobody receives millions of views by posting:

“I increased my retirement contribution by 3%.”

Instead, attention goes to:

luxury hotels

supercars

shopping hauls

expensive watches

private jets

The problem is that consumption produces better content than compounding does.

Investments are boring.

Compound interest is invisible.

Index funds don’t photograph well.

Businesses growing retained earnings rarely trend.

As a result, social media often creates the illusion that spending is the primary evidence of success.

Financial statements tell a very different story.

Real Wealth Buys Choices, Not Just Possessions

People often associate wealth with buying more.

Yet many wealthy individuals describe freedom rather than consumption as the greatest benefit.

Freedom to:

choose meaningful work

take career risks

care for family members

retire earlier

survive economic downturns

ignore toxic workplaces

invest patiently

These freedoms rarely appear in luxury advertisements.

But they may be the most valuable returns wealth produces.

Money becomes most powerful when it increases optionality rather than merely increasing consumption.

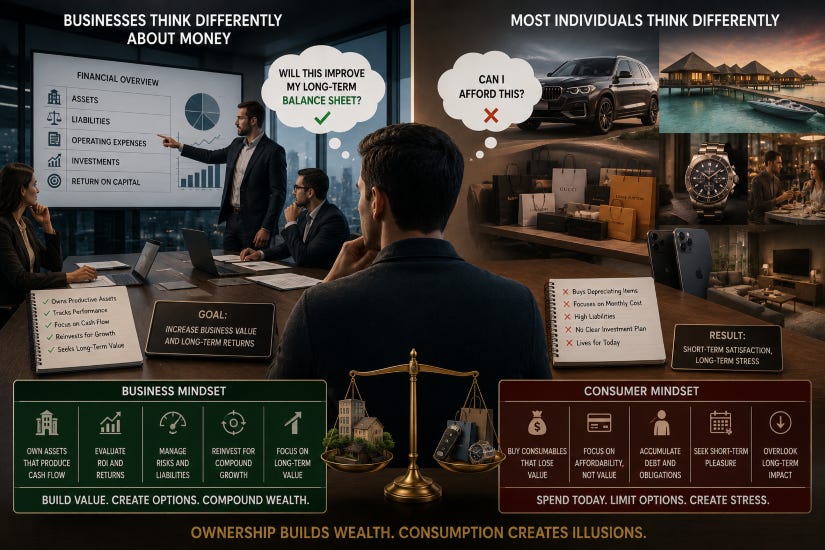

Why Businesses Think Differently About Money

Companies provide an interesting lesson for individuals.

Successful businesses distinguish carefully between:

assets

liabilities

operating expenses

investments

return on capital

Individuals often don’t.

Imagine if households evaluated purchases like corporate investment committees.

Instead of asking:

“Can I afford this?”

They might ask:

“Will this improve my long-term balance sheet?”

That single question dramatically changes purchasing decisions.

Businesses become valuable because they own productive assets.

Households become financially stronger for the same reason.

Practical Lessons You Can Apply This Week

Building wealth rarely requires dramatic changes.

Small structural decisions repeated consistently matter far more.

Consider these habits:

Measure your net worth every six months instead of judging progress by income alone.

Before making a large purchase, ask whether it increases consumption or ownership.

Treat salary increases as opportunities to raise investment rates before raising lifestyle costs.

Build liquidity alongside long-term investments, so unexpected expenses don’t force poor decisions.

Spend intentionally on experiences and products that genuinely improve your life, not simply those that signal success to others.

Review your personal balance sheet with the same seriousness a business reviews its financial statements.

None of these habits is glamorous.

That is precisely why they work.

The Quiet Difference

Looking rich attracts attention.

Becoming wealthy creates resilience.

One depends on other people’s perceptions.

The other depends on your own balance sheet.

One is measured by visible spending.

The other is measured by ownership, cash flow, liquidity, and time.

Perhaps the most surprising lesson is that the two goals often compete with each other.

Every rupee spent proving financial success is a rupee that cannot compound.

Every productive asset quietly accumulated increases future choices that nobody else can see.

In the end, wealth isn’t the ability to purchase expensive things.

It’s the ability to own enough productive assets that your future depends less on your next paycheck and more on what your capital is quietly earning while nobody is watching.

If you enjoy understanding the behaviour behind money, you will love seeing how it all connects to the bigger picture too. Every Wednesday and Saturday, I break down markets, inflation, RBI moves, and real opportunities in my other publication - The Finance Lens. It’s a simple, clutter-free way to stay ahead without drowning in noise.

You can read the latest edition here:

Thanks for reading. Until next time, keep building wealth that lasts not just success that shows.

Your support means a lot-please subscribe, like, and share if you found value here.

💛Smita

Very good read, thanks for sharing!!

You are simply awesome in putting thoughts in right perspective & showing a comparative thought & analysis is so real that we feel day in day out.!! My next question is why our traditional indian thinking ( Marwadi kind) was like this, how did it not withstand the onslaught of capitalism, consumerism, market forces just 1.5 decade 1991-2005? Was it so fragile that the demonstration effect of goods/materials item was so strong that it demolished our traditional wisdom, or our deferred gratification surrendered to instant gratification. I mean something is missing in making us victim. Either globalization was a precursor of things like we have or our IT services industry pushed it or is it a timely combination of all the forces? Would love to discuss, learn from your deep insights about us, our polity, economy, sociology, psychology and what not. Thanks for sharing such detailed analysis. My friend called me after reading & had become fan of your writings !! All the best !!

Narender